Settlements balance liquidity delivery with safeguards to protect traders and minimise risks.

How Settlements Work

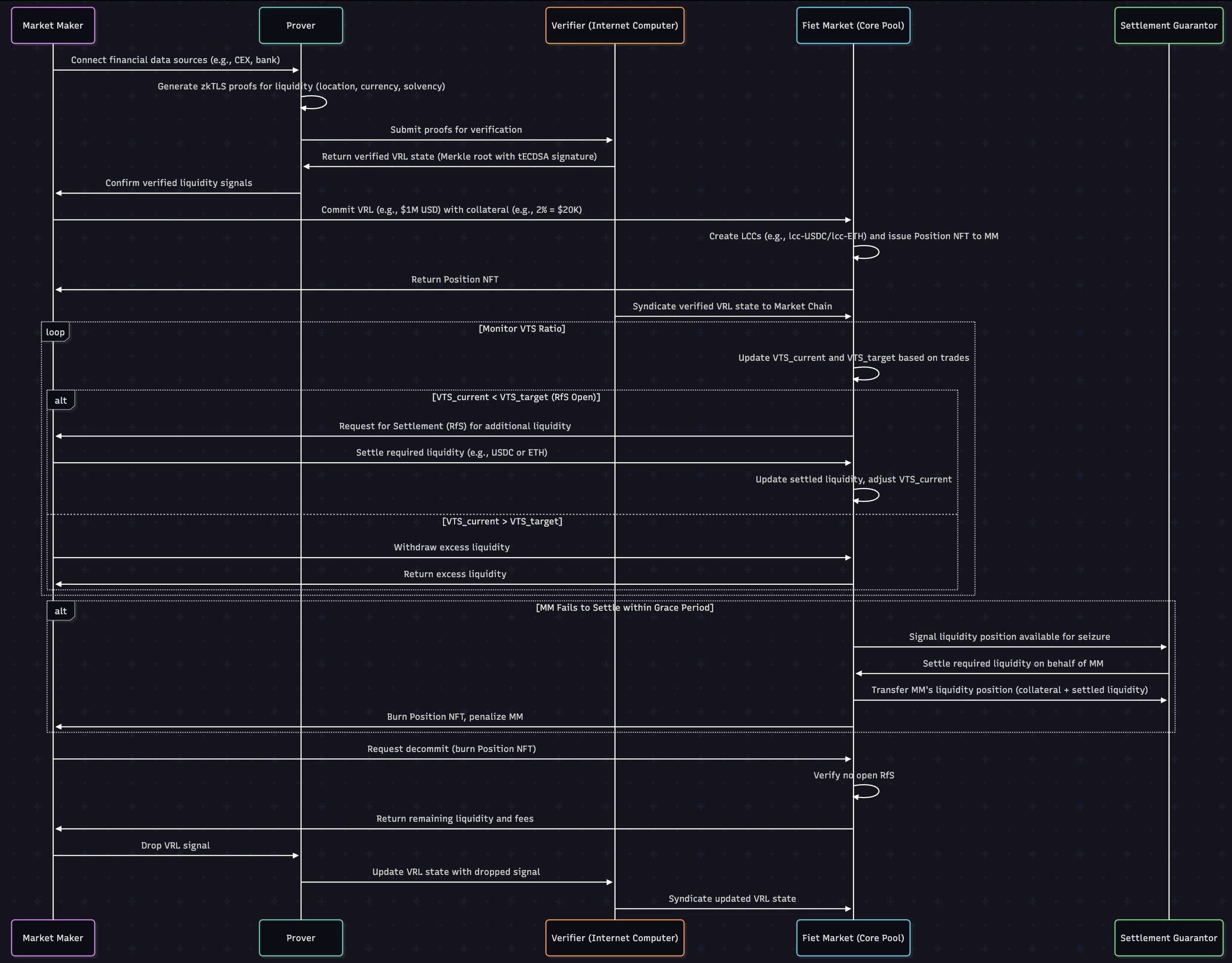

An RfS is triggered when the VTS ratio for a currency falls below its target, indicating a liquidity shortfall. Market makers must settle the required amount, proportional to their VRL commitment, within a fixed grace period (set at market deployment, e.g., based on bank transfer times). If they fail, settlement guarantors — other market makers or bots — can settle on their behalf, seizing the failing market maker’s collateral or liquidity position as profit. This incentivises timely delivery while ensuring market continuity.Managing Settlement Risk

Fiet mitigates settlement risk through multiple safeguards:- Collateralisation: Market makers deposit a base VTS collateral (e.g., 2% of their commitment) on-chain, securing their obligations and incentivising guarantors to intervene if needed.

- Seizure Mechanism: After the grace period, a failing market maker’s position is seizable on a linear scale (e.g., fully seizable after an hour), ensuring guarantors act swiftly to restore liquidity.

- Proof of Settlement: Market makers can submit zkTLS-verified proof of pending settlements (e.g., a bank transfer) to extend the grace period, reducing seizure risk during delays.

- Looping: Guarantors with smaller reserves can partially settle and seize proportional positions, iterating until the RfS is fulfilled, broadening participation.

Protecting User Funds

Traders’ funds are protected by Fiet’s non-custodial design and protocol-bound LCCs:- Non-Custodial: Traders retain control of their assets, swapping LCCs in the DEX without Fiet holding funds.

- LCC Restrictions: LCCs are non-transferable, locked to Fiet’s DEX, preventing misuse or external risks.

- Guarantor Backstop: If a market maker fails, guarantors deliver liquidity, ensuring traders receive their swapped assets.

- Collateral Buffer: The base VTS collateral absorbs potential shortfalls, protecting traders from losses.

Fiet’s non-custodial design and guarantor system safeguard user funds against settlement failures.

Sequence Diagram

Guarantor Incentive Structure

The following scenario offers a breakdown of the incentive structure that guarantees settlements to Fiet Markets.

Context

In an AMM pool with virtual and realised liquidity, MMs deposit a base collateral equal to 2% of their committed liquidity per currency. Consider a USDC/XYZ pool, with = $1,000,000, at a 1:1 exchange rate in a 50/50 pool — using a constant sum invariant price algorithm for the sake of simplicity. The pool initially holds:- Realised Liquidity: $10,000 USDC and $10,000 XYZ.

- Virtual Liquidity: $980,000 USD ($1,000,000 total from MMs’ commitments minus realised liquidity)

Calculations

- Trader’s Action: Deposits $100,000 USDC, withdraws $100,000 XYZ.

- Pool’s Realised Liquidity Before Settlement:

- USDC: $10,000 + $100,000 = $110,000

- XYZ: $10,000 - $10,000 = $0 (pool provides its $10,000 XYZ to trader, shortfall remains $90,000 XYZ)

- MM Settlement: MMs collectively settle $90,000 XYZ

- Realised Liquidity After Settlement

- to Pool: $110,000 USDC, $90,000 XYZ

- to Trader: $110,000 USDC, $0 XYZ

MM A’s Liquidity Position

MM A’s 50% share of the pool’s realised liquidity post-swap is $55,000 USDC (0.5 $110,000) Since the pool has $0 XYZ post-settlement, MM A’s position is valued at $55,000 USDC.Guarantor’s Profit

If MM B settles MM A’s $45,000 XYZ obligation:- MM B seizes MM A’s position: $55,000 USDC.

- Profit = $55,000 USDC - $45,000 XYZ = $10,000 (assuming 1:1 value).

Incentive Mechanism

The base collateral acts as an incentive for guarantors (e.g., MM B) to settle on behalf of a failing MM (e.g., MM A), as the seized liquidity position’s value ($55,000 USDC) exceeds the settlement cost ($45,000 XYZ), yielding a profit equal to the failing MM’s proportional collateral. This ensures market liquidity and operational stability.Learn More

Explore related concepts and details:- Value-to-Signal: See how VTS triggers RfS.

- Liquidity Commitment Certificates: Understand LCCs’ role in settlements.

- Markets: Learn about AMM pools requiring settlements.

- Technical Specification: Review settlement mechanics.

- Join the Community: Discuss settlement risks on Discord.